The Toronto Real Estate Board (TREB) announced that Greater Toronto Area (GTA) REALTORS® reported 92,394 sales through TREB’s MLS® System in 2017. This total was down 18.3% compared to the record sales reported in 2016.

But let’s put the 2017 sales into an historical perspective. Even if we include the record sales of 101,213 in 2015 and 113,040 in 2016 in the equation, the GTA recorded 95,916 sales per year on average over the five year period from 2012 to 2016. Taking that into consideration, 2017’s results are only off by 3.7% from the 5-year average. In addition, there has been only one other year (besides 2015 and 2016) when sales breached the 93,000 mark, and that was in 2007, before the “Great Recession”, when the GTA recorded 93,193 sales.

After record sales in all segments of the market in Q1, the pace of sales decline in Q2 and Q3 after the Ontario Fair Housing Plan (i.e. the foreign buyers tax) was introduced. Q4 brought back some strength to the market as some buyers arguably brought forward their home purchase to beat the introduction in January of 2018 of the changes to the federal mortgage lending guidelines (the “stress test”).

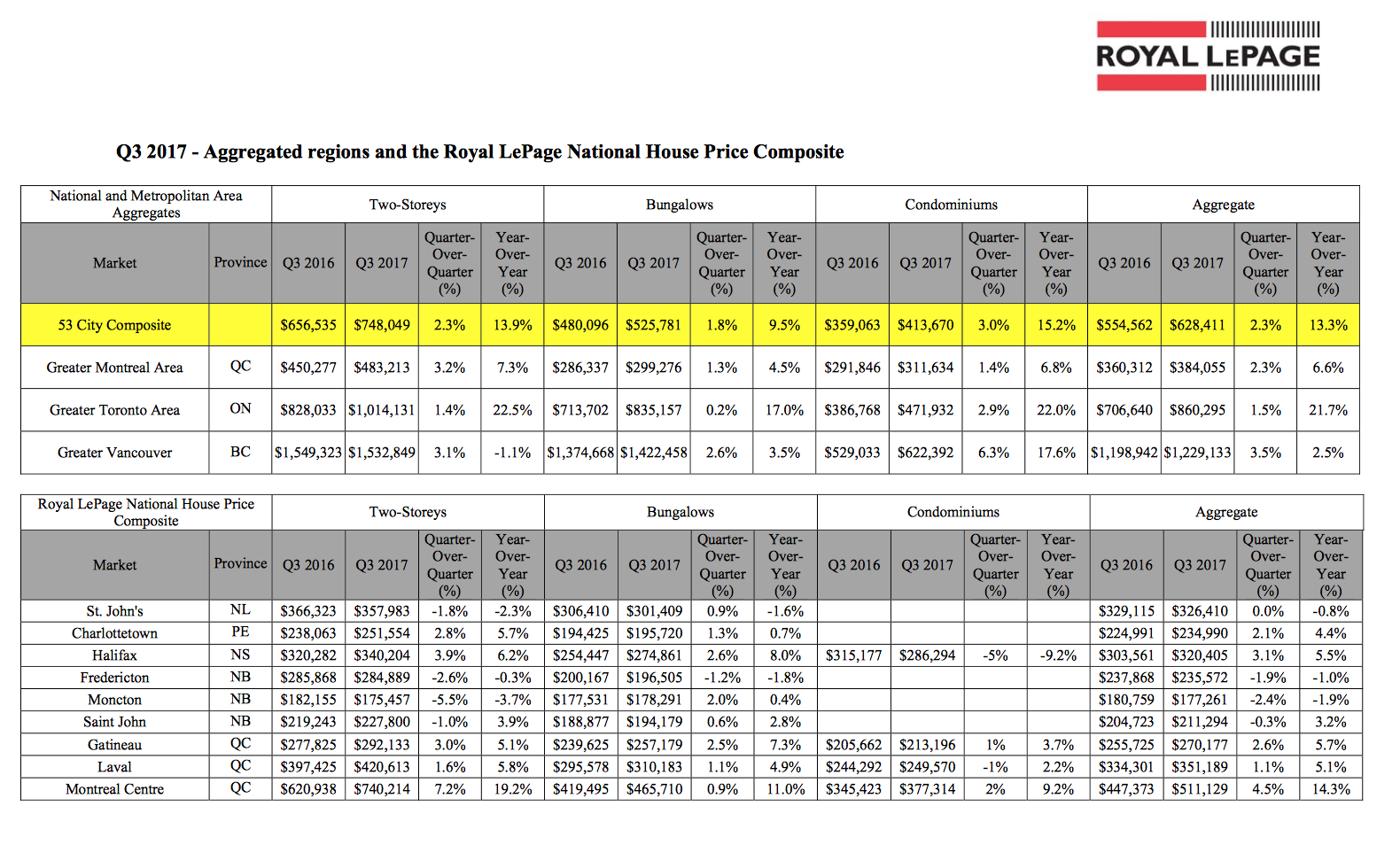

Despite the drop of 20,646 annual sales from the 2016 figure, the average sales price recorded in the GTA for 2017 as a whole rose by 12.7% to $822,681, from $729,837 in 2016, although home price growth in the second half of 2017 differed substantially depending on market segment. The drop was felt primarily in the most expensive detached market segment, where sales dropped by 12,381 homes or 23.0%, but representing almost 60% of the total unit sales decrease of 20,646 units. The average price of a single detached home in the GTA increased in 2017 by 12.7% to $1,098,951, forcing many buyers to look for less expensive options. At the other end of the market spectrum, condominium apartments experienced a drop of 2,853 unit sales, or 9.6%, accounting for approximately 13.8% of the total decrease of 20,646 units, but prices in this segment were up 23.1% from 2016 levels to an average of $512,478 in 2017.

These factors also contributed to the shift in relative share of total sales where the percentage of single detached homes decreased by 2.8% to 44.7% of units sold and the share of condominium apartments rose by 2.8% to 29.1% of total units sold. Expectations are that as more millennials begin to reach the age of home ownership, the trade-off between housing type and location will likely become more prevalent in the future across the GTA and this will also place a significant strain on inventory, turning the process of finding a home into an exercise in adjusting expectations.

According to Royal LePage’s most recent Market Survey Forecast, the company predicts that the aggregate price of a home in the GTA will appreciate by 6.8% by the end of 2018, as many purchasers become acclimatized to the new mortgage rules and continue to compete over low inventory levels, particularly in the condominium market where demand significantly exceeds supply due to the long lead times in building these units.

If you are curious to know how much your property is worth today or how much you can afford to buy, please feel free to reach out; and if you found this article helpful please hit "Like" and "Share".