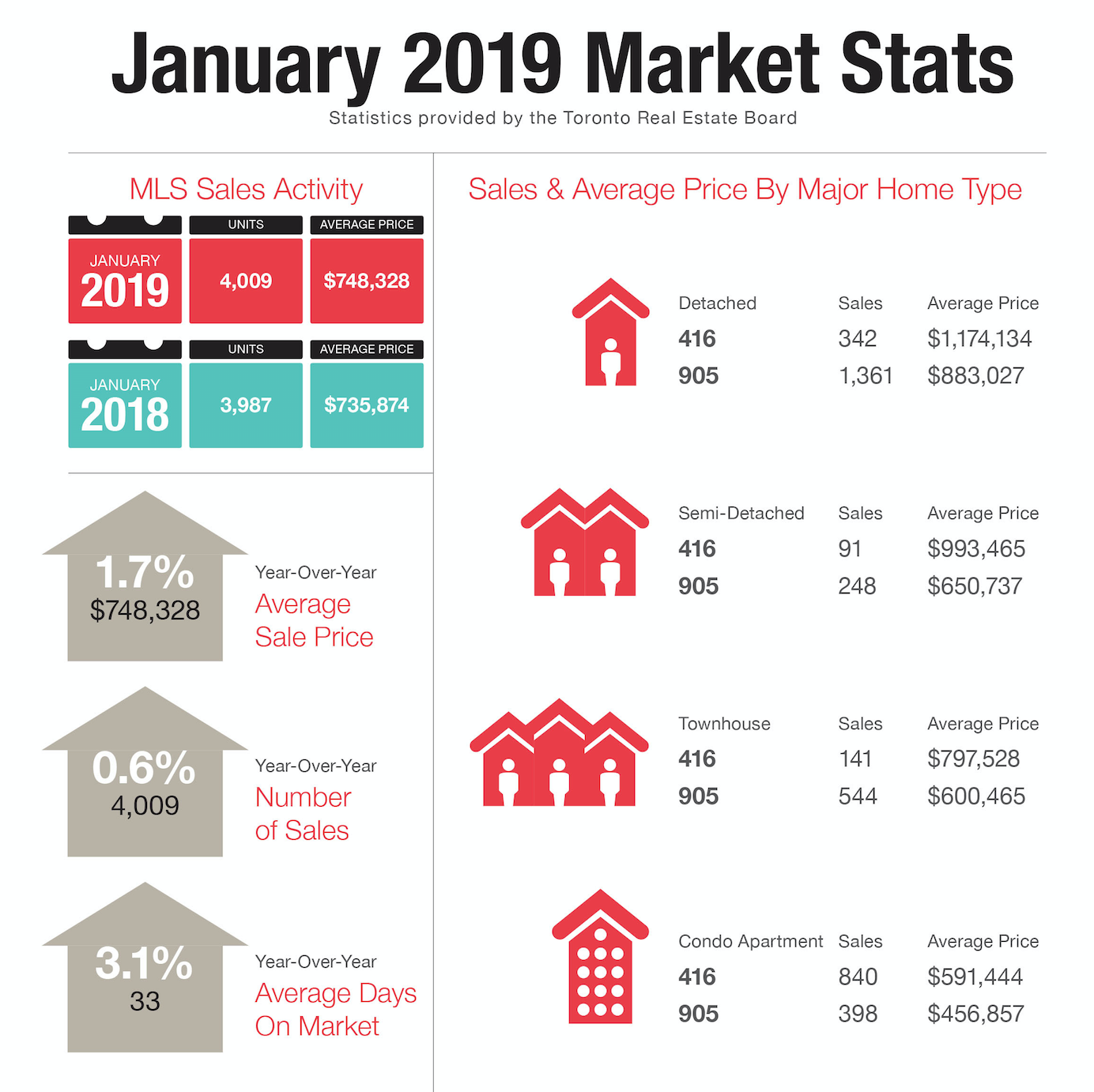

Is It Better to Rent or Buy in 2025? Canadian Renters Are Strategizing

The rent vs. buy debate is alive across Canada, and renters are paying close attention.

TORONTO, June 19, 2025 – As interest rates decline and the supply of homes for sale grows, affordability is improving, shifting many residential real estate markets across the country in favour of buyers. This would seem to open the door for renters considering the move to home ownership. However, behaviour is more nuanced and many are approaching the opportunity strategically.

According to a new national survey by Royal LePage, 54% of renters say they plan to purchase a home in the future. Nearly one-third of those plan to buy within the next five years. But in a housing market shaped by fluctuating mortgage rates and softening home prices, many are playing it smart, not fast.

Why Are Renters Holding Off on Buying a Home?

Across the country, 28% of renters say they considered buying before signing their current lease. What stopped them?

40% are waiting for home prices to decline

29% are watching for further interest rate cuts

28% are continuing to save for a down payment

This isn’t fear—it’s strategy. Many are weighing affordability, lifestyle, and timing as Canada’s housing market enters a transitional phase.

Rental Affordability Remains a Pressure Point

Even with national rent prices dropping for eight straight months, affordability remains tight. According to the Rentals.ca and Urbanation report:

Average one-bedroom rent in Canada (May 2025): $1,857 (↓ 3.6% YoY)

Average two-bedroom: $2,225 (↓ 4.6% YoY)

Yet 52% of tenants spend over 30% of their income on rent. Many are cutting back on essentials, savings, or taking second jobs to stay housed.

Ontario Snapshot: Renters Still Watching the Market

In Ontario, 28% of renters also considered buying before renewing their lease.

Top reasons they stayed in the rental market:

43% are waiting for home prices to drop

34% are watching interest rates

34% couldn’t qualify for a mortgage

Still, 55% plan to buy:

But 31% say homeownership isn’t part of their plan. Half cite income limitations for the neighbourhoods they want to live in. Another 43% say renting is still more affordable, and 43% don’t want the responsibilities of home maintenance.

Toronto Rental Market – May 2025 Update

In Toronto, a surge of new condo completions has added welcome inventory to the rental market. This supply boost, combined with lower student visa and work permit numbers, has softened demand and cooled the bidding wars that became common in 2022–2023.

But activity is returning in pockets of the city—especially in and around the Financial District, where many employers are now requiring in-person work. One-bedroom units with dens remain highly sought after, particularly in vibrant areas with green space and amenities.

📍 Toronto Rental Prices – May 2025

One-bedroom average: $2,302 (↓ 7.1% YoY, ↓ 0.7% MoM)

Two-bedroom average: $2,933 (↓ 10.7% YoY, ↑ 0.3% MoM)

How Ontario Renters Are Stretching to Afford Rent

38% spend 31–50% of income on rent

15% spend more than 50%

39% reduced spending on food

32% cut retirement/savings

22% have credit card debt linked to rent

Even with price drops, the cost of renting is still high—and the long-term burden is real.

Please read the full report: HERE

Royal LePage 2025 Canadian Renters Report – Data Chart: rlp.ca/2025-Canadian-Renters-Report-Chart

Will Renting or Buying Make More Sense in 2025?

With builders pulling back on new construction, the current uptick in rental supply may be short-lived. Analysts expect reduced housing starts in 2027–2028, which could lead to another surge in demand—and higher prices down the line.

That makes the present a unique window. For some, it’s a chance to upgrade rentals. For others, it may be the perfect time to explore homeownership before the market tightens again.

Need Help Deciding Whether to Rent or Buy in 2025?

Every renter’s situation is unique. If you’re watching interest rates, housing prices, or mortgage options and wondering what move to make—I’m here to help.

Let’s map out your real estate goals, your affordability zone, and what opportunities exist in your area. Whether you’re planning to buy next month or next year, clarity starts now.

— Luba

I offer Private 1:1 Real Estate Clarity Calls

Whether you're looking to sell soon, debating renos, or just want a second opinion before making a move—this is where we cut through the noise.

In a sea of opinions, I offer grounded perspective. In a market full of noise, I offer clarity. If you've been spinning in circles, this is where things start to make sense.

This isn't a sales pitch. It's a clarity session. You bring the questions. I bring grounded experience—rooted in trust and truth. Together, we map out your smartest next move—saving you time, money, and unnecessary stress.